2 Credits

and Debits 2

1.1 What are Debits and Credits? 2

1.2 What Is An Account? 2

1.3 Double-Entry Accounting 2

1.4 Debits and Credits 2

2 T-Accounts 5

2.1 Journal Entries 6

2.2 When Cash Is Debited and

Credited 6

3 Normal Balances 8

3.1 Revenues and Gains Are Usually

Credited 8

3.2 Expenses and Losses are Usually

Debited 9

3.3 Permanent and Temporary Accounts 9

4 Bank's Debits and Credits 11

4.1.1 Transaction

#1 11

4.1.2 Transaction

#2 11

4.1.3 Transaction

#3 12

4.2 Bank's Balance Sheet 13

4.3 Recap 13

Debits and credits are terms used by bookkeepers and accountants when

recording transactions in the accounting records. The amount in every

transaction must be entered in one account on the left as a debit and in at

least one other on the right as a credit. This is double-entry bookkeeping –

for accuracy in the accounting records, used for managing the business and

producing the financial statements (for investors amongst others).

But which account gets the debit entry and which the credit entry? First,

let’s look at the accounts where debits and credits are entered or “posted” and

T-bars that aid communication….

Account are a way of organising all the transactions into groups, or “accounts”

or “ledgers”. When a company's accounting system is set up, the accounts most

likely to be needed are identified and listed out in the chart

of accounts.

Within the chart of accounts the balance sheet accounts are listed first,

followed by the income statement accounts:

“Double” because every business transaction affects at least two

accounts.

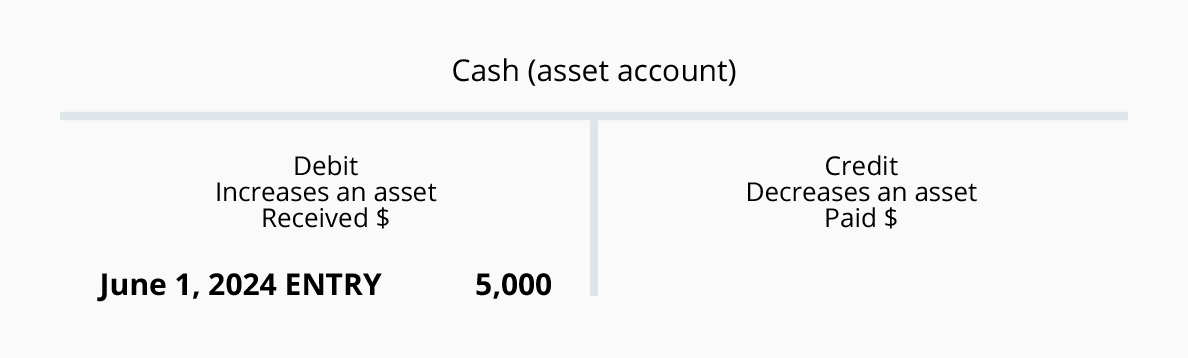

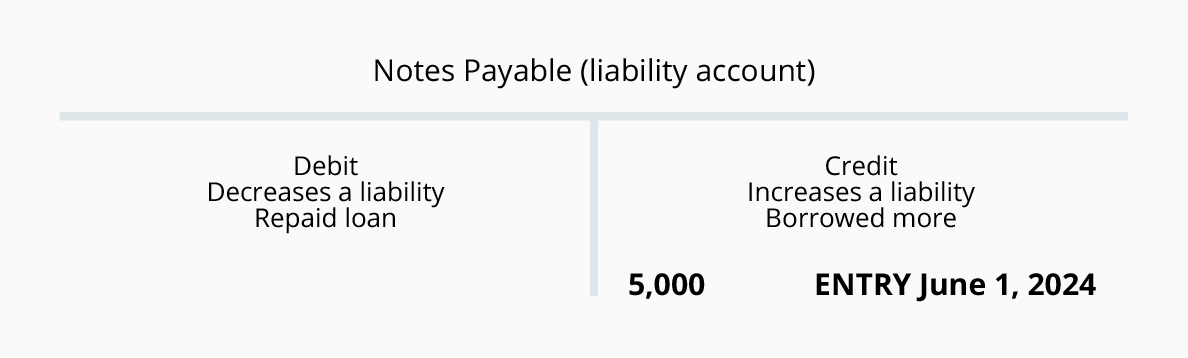

For example, when a company borrows 1,000, the transaction will hit the

company's Cash account (as a debit) and Notes Payable account (credit). Then

monthly repayments will come out of cash (credit), debit Notes Payable to reduce

the balance due, but also there will be a third account: Interest Expense to increase,

debit.

Accounting software will automatically reduce your Cash account and the

prompt you for the other accounts.

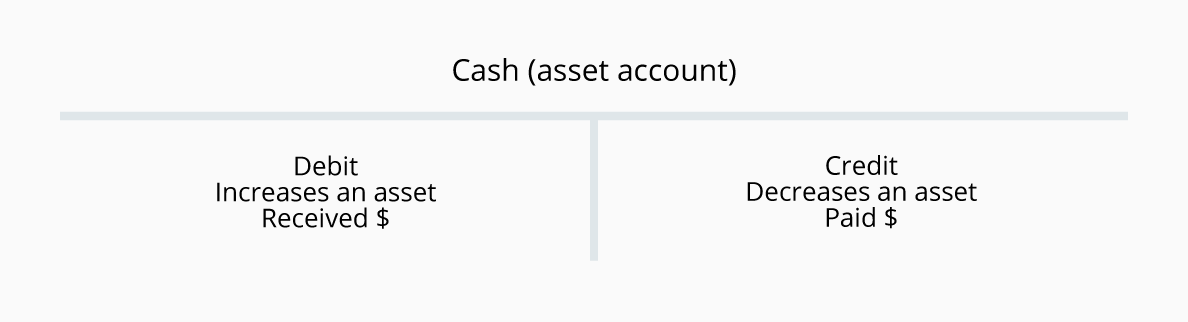

To debit an account means to enter an amount on the left side of the

account. To credit an account means to enter an amount on the right side.

Generally, these accounts are increased with a debit:

Dividends (Draws)

Expenses

Assets

Losses

D - E - A - L are increased with a debit.

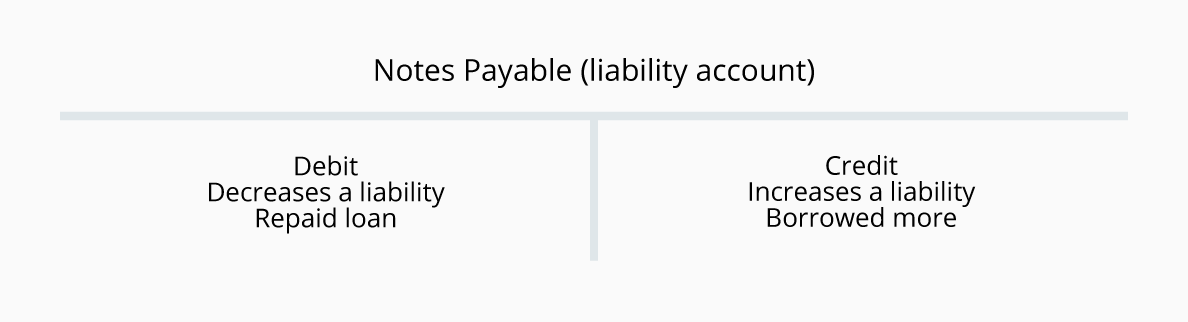

Generally, the following types of accounts are increased with a

credit:

Gains

Income

Revenues

Liabilities

Stockholders' (Owner's) Equity

G - I - R - L - S are increased with a credit.

The abbreviation for debit is dr. and the abbreviation for credit is cr.

|

ASSETS

|

LIABILITIES

|

EQUITY

|

REVENUE

|

EXPENSES

|

|

DEBIT

|

↑ increase

|

↓ decrease

|

↓ decrease

|

↓ decrease

|

↑ increase

|

|

CREDIT

|

↓ decrease

|

↑ increase

|

↑ increase

|

↑ increase

|

↓ decrease

|

DC ADE LER

DC ADE LER

After doing a few T-bars, it will come intuitively.

Up to you how you

remember …

T-bars are a great visual aid to see the effect of a transaction or journal

entry.

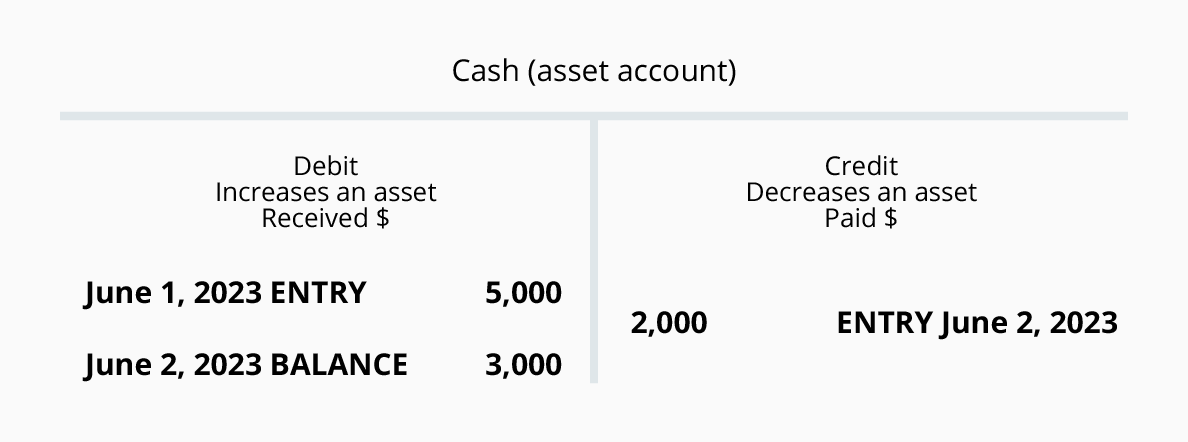

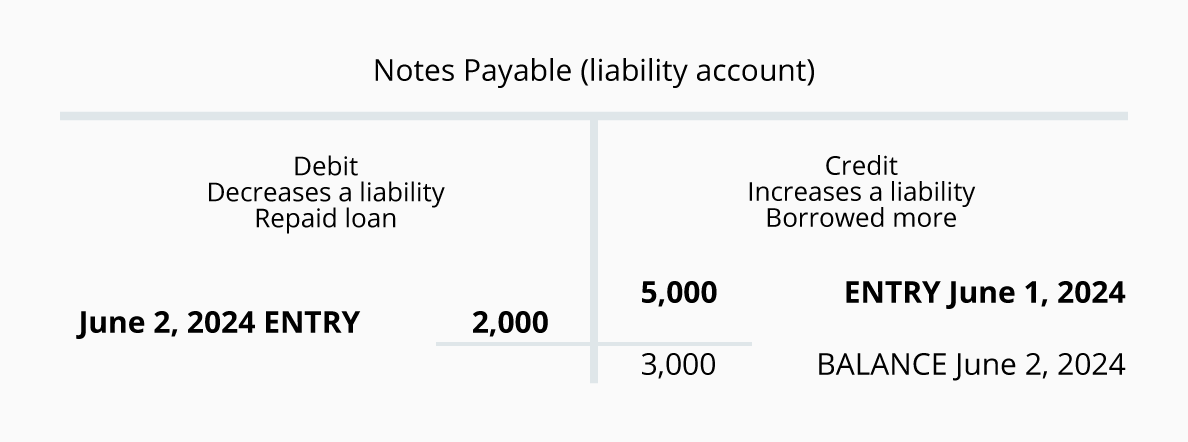

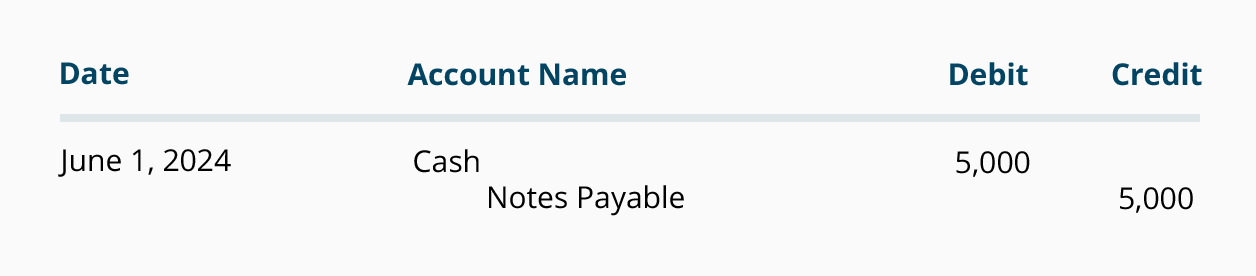

Take out and repay a loan – hits accounts Cash and Notes Payable.

1.

Receive a loan, increase cash, increase loans repayable

- Debit Cash, Credit Notes Payable:

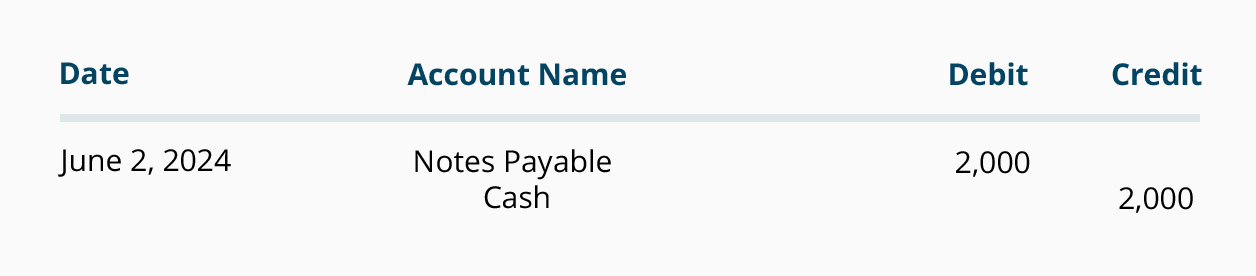

2.

Repay the loan, decrease cash, decrease notes

payable – Credit Cash, Debit Notes Payable

Those are T-bars, but you can visualise business transactions vy writing

general journal entries. Look at what is required for a JE.

To set off on the right foot, memorise the following:

- Whenever

cash is received, debit Cash.

- Whenever

cash is paid out, credit Cash.

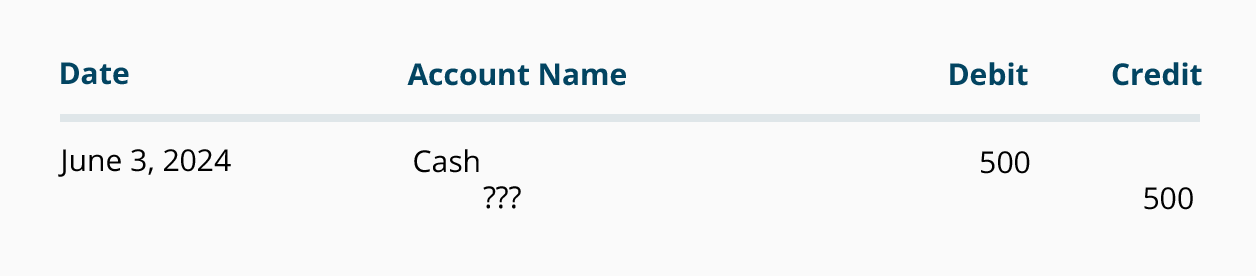

Imagine that a company receives $500 from a customer who was given 30

days in which to pay. (Previously, the company had recorded the sale and an

accounts receivable.) So the company will debit Cash, because cash was

received. The amount of the debit and the credit is $500. The general journal

format is:

Which account is to be credited? Since this was the collection of an account

receivable, the credit should be Accounts

Receivable. (Because the sale was already recorded, you cannot

enter Sales

again.)

Whenever cash is paid out, the Cash account is credited (and another

account will have to be debited).

Where would you look in an account to see how much is in it? When looking at

an account in the general ledger, or GL, you would normally find the

debit or credit balance here:

Revenues and gains are recorded in accounts such as Sales, Service

Revenues, Interest

Revenues (or

Interest Income), and Gain

on Sale of Assets.

These accounts normally have credit balances that are increased with a credit

entry. In a T-account, their balances will be on the right side.

However, the exceptions to this rule are whare called “contra accounts”,

contra = against. Sales

Returns, Sales

Allowances, and Sales

Discounts - these

accounts have debit balances because they are reductions to sales.

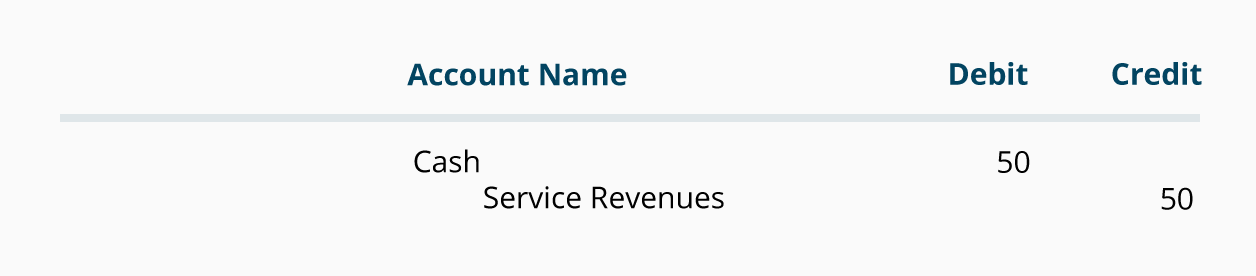

For example, if you perform a service and immediately get paid the full

amount $50:

The asset account Cash is debited and the revenue account Service Revenues will

immediately be credited, increasing its account balance, because you completed

the service and were paid all at the same time.

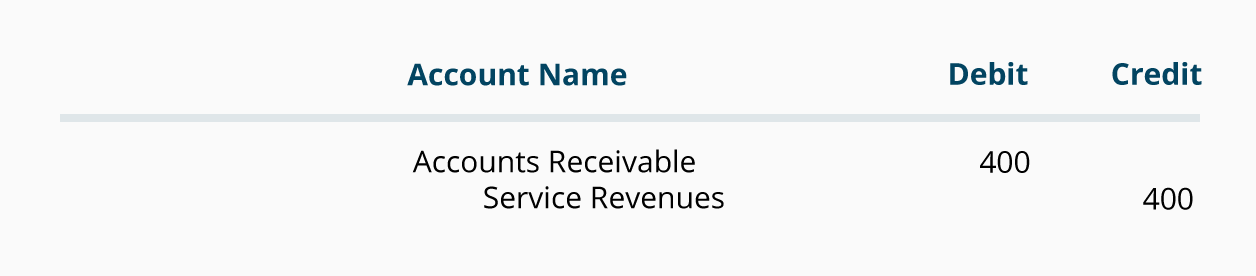

But if a company performs a service on credit? (i.e., the company

allows the client to pay for the service at a later date, such as 30 days from

the date of the invoice).

At the time the service is performed the revenues are considered to have

been earned and so they are recorded in the revenue account, Service Revenues,

with a credit. The other account involved cannot be the asset Cash as cash was not

received.

The account to be debited is the asset account Accounts Receivable, en

attendant. If the amount of the service performed is $400, the entry in journal

entry JE format is:

Accounts Receivable, as an asset account, and is increased with a debit;

Service Revenues, a revenue account, is increased with a credit.

Expenses

normally have debit balances and are increased with a debit entry. Since

expenses are usually increasing, think "debit" when expenses are

incurred. (We credit expenses only to reduce them, adjust them, or to close

the expense accounts.) Examples of expense accounts include Salaries

Expense, Wages

Expense, Rent

Expense, Supplies

Expense, and Interest

Expense. In a

T-account, their balances will be on the left side.

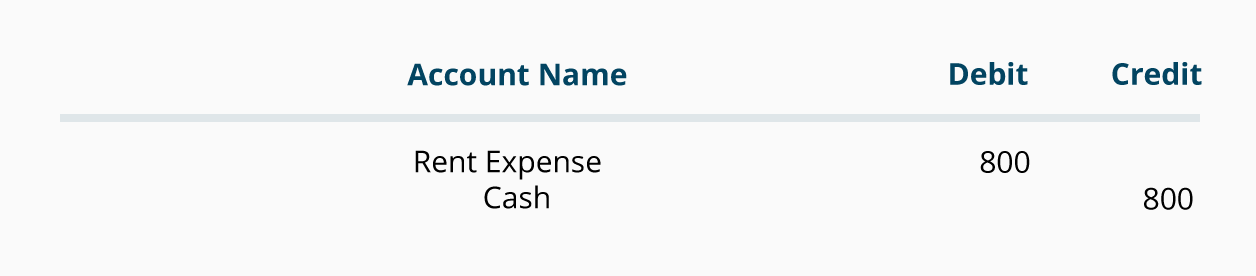

For example, pay $800 to the landlord for rent:

(Debits before credits in JE format, credit is indented.)

Cash is credited and Rent Expense is debited. (If the payment was made in advance

of the month, the debit would go to the asset account Prepaid

Rent.

To increase an expense account, debit the account.

Asset, liability, and most owner/stockholder equity accounts are referred to

as "permanent accounts" (or "real accounts").

Permanent accounts are not closed at the end of the accounting year; their

balances are automatically carried forward to the next accounting year.

"Temporary accounts" (or "nominal accounts" they

are also called) include all the revenue accounts, expense accounts, the

owner's drawing account, and the income summary account. Usually, the balances

in temporary accounts increase throughout the accounting year. Then at the end

of the accounting year the balances are transferred to equity - the owner's

capital account or a corporation's retained earnings account.

By transferring out the balances on temporary accounts at the end of the

accounting year, each temporary account will have a zero balance for when the

next accounting year begins. Ie, the new accounting year starts with no revenue

amounts, no expense amounts, and no amount in the drawing account.

It is by having many revenue accounts and many many expense accounts that a

company is able to report detailed info on revenues and expenses throughout the

year.

When you hear your banker say, "I'll credit your

bank account," it means the transaction will increase your checking

account balance. Conversely, if your bank debits your account (e.g.,

takes a monthly service charge from your account) your account balance

decreases.

We learned that debiting the Cash

account in the general ledger GL increases its balance, yet your bank

says it is crediting your bank account to increase its balance ???

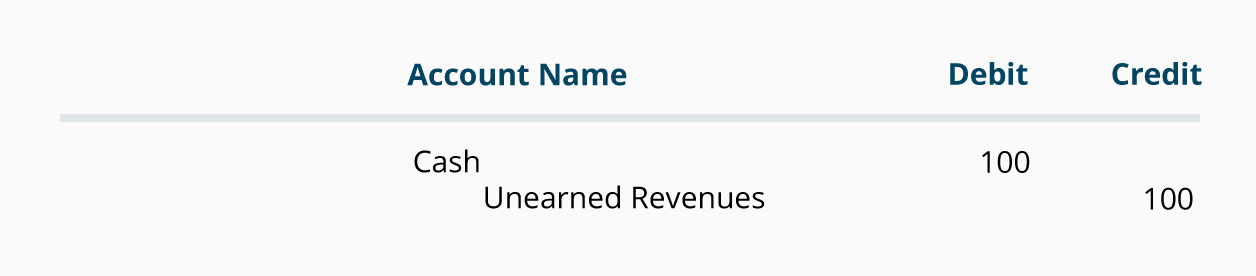

Let's say that your company, Debris Disposal, receives $100

of currency from a customer as a down payment for a future site clean-up

service. When the money is received, your company makes the following entry:

(Debris Disposal's journal entry)

Debris Disposal increases Cash account with a debit of $100.

Since the company has not yet earned the $100, it cannot credit a

revenue account. Instead, the liability account Unearned Revenues is credited -

Debris Disposal has a liability to do the work (or to return the $100). Note: an

alternate title for the Unearned Revenues account is Customer

Deposits.

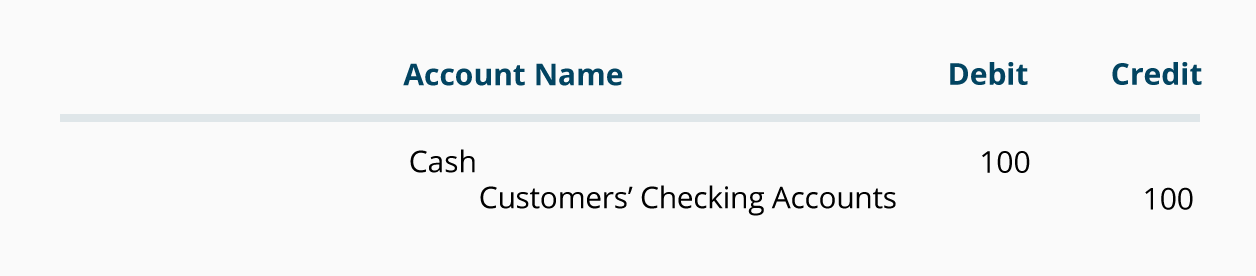

Now let's say you take that $100 to Trustworthy Bank and

deposit it into Debris Disposal's bank account. Since Trustworthy Bank is

receiving cash, the bank debits its general ledger Cash account for $100, increasing

the bank's assets. The rules of double-entry accounting require the bank itself

to also enter a credit of $100 into another of the bank's general ledger

accounts. Because the bank has not earned the $100, it cannot credit a

revenue account. Instead, the bank credits a liability account such as

Customers' Bank Accounts, reflecting the bank's obligation/liability to return

the $100 to Debris Disposal on demand.

In general journal format, these are the JEs the bank makes

to record this transaction:

As the entry shows, the bank's assets increase by the debit

of $100 and the bank's liabilities increase by the credit of $100. And in the

bank's detailed records, Debris Disposal's current account is the specific

liability that increased.

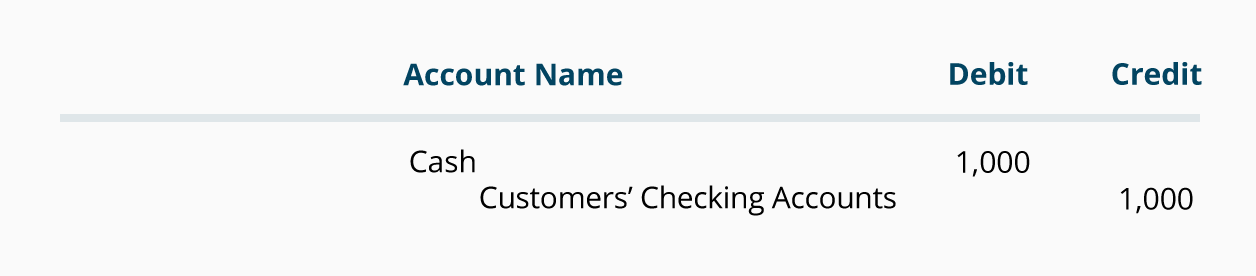

Now let's say Trustworthy Bank receives a $1,000 transfer on

your company's behalf from a person who owes money to Debris Disposal. Two

things happen at the bank:

The bank receives $1,000, and

The bank records its obligation to give the money to Debris

Disposal on demand.

Trustworthy Bank's journal entries:

The debit increases the bank's assets by $1,000 and the

credit increases the bank's liabilities by $1,000. (And the bank's detailed

records show that Debris Disposal's current account is the specific liability

that increased.)

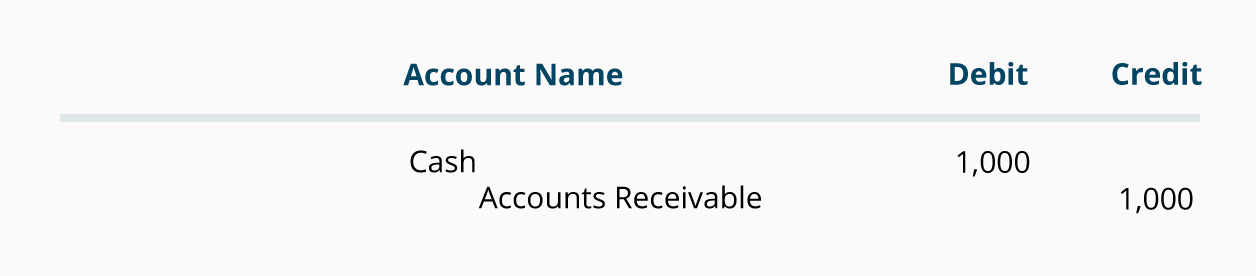

At the same time, the $1,000 transfer is received at the

bank, Debris Disposal makes the following entry into its general ledger:

(Debris Disposal's journal entry)

As a result of collecting $1,000 from one of its customers,

Debris Disposal's Cash balance increases and its Accounts Receivable balance

decreases.

Many banks charge a monthly fee on checking accounts. If

Trustworthy Bank decreases Debris Disposal's current account balance by $13.00

to pay for the bank's monthly service charge, this might be itemized on Debris

Disposal's bank statement as a "debit memo" – the bank gets the money

so it is a debit from the bank’s point of view.

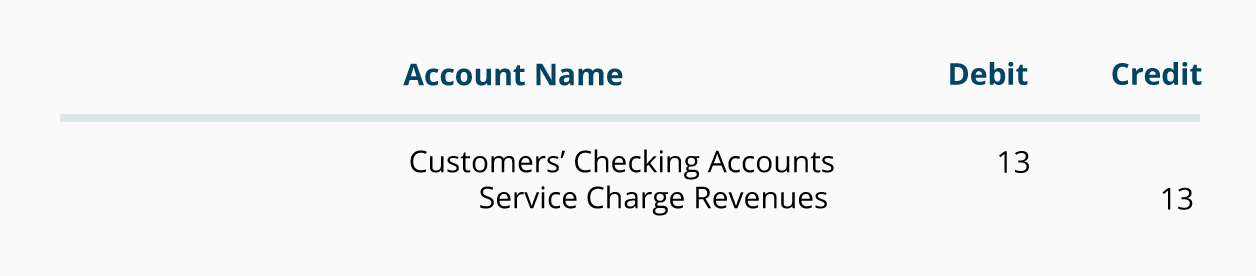

The entry in the bank's records will show the bank's

liability being reduced (because the bank owes Debris Disposal $13 less). It

also shows that the bank earned revenues of $13 by servicing the checking

account.

The Bank's GL general ledger:

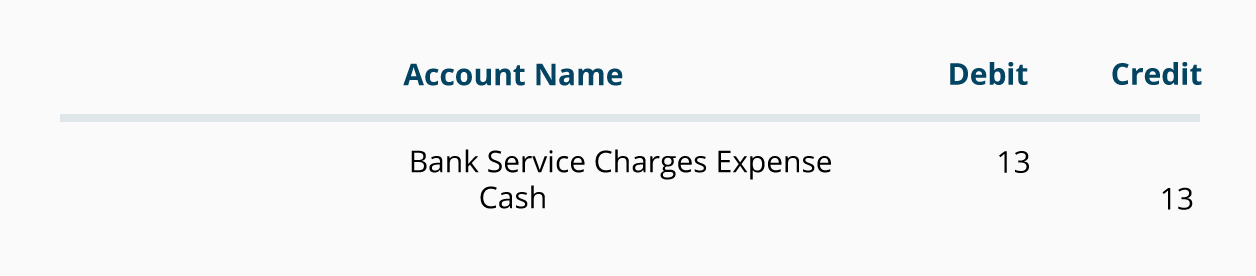

On your company's records, par contre, the entry will look

like this:

Debris Disposal's GL general ledger:

Debris Disposal's cash is reduced with a credit of $13 and

expenses are increased with a debit of $13. (Note: if the amount of the bank's

service charges is not significant a company may debit the charge to Miscellaneous

Expense.)

Accounts such as Cash, Investment

Securities, and Loans

Receivable are reported as assets on the bank's balance sheet.

Customers' bank accounts are reported as liabilities and include the balances

in its customers' checking and savings accounts as well as certificates of

deposit. In effect, your bank statement is just one of thousands of

subsidiary records that account for millions of dollars that a bank owes to its

depositors.

Recapping so far:

·

Debit means left

·

Credit means right

·

Every transaction affects two accounts or more

·

At least one account will be debited and at

least one account will be credited

·

The total of the amount(s) entered as debits

must equal the total of the amount(s) entered as credits

·

When cash is received, debit Cash

·

When cash is paid out, credit Cash

·

To increase an asset,

debit the asset account

·

To increase a liability,

credit the liability account

·

To increase owner's

equity, credit an owner's equity account

·

To increase revenues,

credit the revenues account

·

A credit to a revenue account also causes an

increase in owner's equity

·

To increase expenses,

debit the expense account

·

A debit to an expense account also causes a

decrease in owner's equity.